The house feels different. Not emptier in a sad way, just lighter. Without the constant hum of piano lessons and late-night snacks, there’s suddenly space (literally and figuratively) to think about what comes next.

Welcome to the empty nest stage: one part financial reset, one part lifestyle shakeup. Empty nesting isn’t a pause, but a pivot point. Routines loosen, priorities shift, and the next chapter starts looking like an opportunity to embrace both responsibility and freedom. With a clear plan, this stage can be a launchpad for smarter financial choices, new adventures, and a life that’s both secure and fulfilling.

Stretching the Freed-Up Dollars

Empty nesting has a way of slimming down the monthly bills. Grocery runs shrink, insurance costs drop once the extra cars are off the policy, and utility bills finally take a breather. And if tuition is behind you too? That’s real financial elbow room.

The question becomes: where should that money go now? The short answer is that it’s different for everyone, depending on your unique situation and financial priorities. Some smart ways to allocate those funds include:

Boost retirement savings while you’re still in peak earning years.

Pay off the mortgage faster, if you want to head into retirement debt-free.

Rebuild the emergency fund, because adult kids do occasionally “boomerang” back.

The important thing is not letting those freed-up dollars disappear into lifestyle creep (the sneaky tendency to upgrade vacations, cars, or impulse buys without a plan).

In addition to looking at how empty nesting affects the monthly budget, this is a great moment to zoom out and check the bigger picture. Questions to consider:

Are your investment accounts aligned with your long-term goals?

Is insurance coverage still the right fit, or is it time to adjust?

Do wills, trusts, and beneficiary designations reflect current wishes?

Balancing the immediate savings windfall with a thoughtful look at long-term priorities helps ensure this stage isn’t just about trimming costs but building freedom and security.

Do You Really Need All This Space?

The empty nest raises a classic debate—downsize or stay put?

Some people love shedding square footage: fewer rooms to clean, lower property taxes, less maintenance. Others keep the family home because they like having space for holidays, grandkids, or the occasional adult child who needs to land temporarily.

There’s no right answer. Downsizing can free up cash and simplify life, but staying put has its comforts. The key is running the numbers to make sure the choice fits long-term goals, not just sentiment.

More Time, More Freedom (and Maybe More Travel)

When kids are grown, money isn’t the only thing that shifts. Time does too. Suddenly weekends aren’t filled with carpools, sports schedules, and college visits. Many empty nesters use this stage to:

Travel more often, and not just during school breaks.

Pick up hobbies that were sidelined years ago.

Volunteer or get more involved in community life.

Even take on “second act” careers or part-time work that feels more fulfilling than the old 9-to-5 grind.

In other words, this stage can be less about winding down and more about leaning into the things that were waiting in the wings.

Expect a Few Surprises

Of course, not every nest stays empty. Some young adults move back home while figuring out their careers, saving for a house, or navigating life changes. And sometimes, supporting aging parents becomes part of the mix too.

As always, the key is to plan with flexibility. Extra savings, reduced debt, and clear goals create a cushion, so those surprises don’t knock everything off course.

Take the Next Step

Handled well, this stage isn’t about downsizing life, it’s about upgrading it. It’s an opportunity to reimagine what comes next for both your life and your finances. But making the most of it takes more than just trimming expenses or daydreaming about travel. It requires a clear, comprehensive plan.

Whether you’re considering downsizing, shoring up retirement savings, or simply deciding how to put those “extra” dollars to work, having a trusted guide can help ensure this next chapter is not only exciting but financially secure. Get in touch with Four Leaf Financial Planning to start the conversation.

Life has a way of throwing curveballs. Sometimes they come in the form of a new job, a move, or retirement plans. Other times, it’s a health challenge that changes how (and even if) you can work. For people on disability benefits, thinking about returning to work can feel intimidating. There are earnings limits, reporting requirements, and a lot of “what ifs.” On the other hand, part-time work can open doors, not just to income, but to purpose, connection, and confidence, too.

Understanding SSDI

Social Security Disability Insurance (SSDI) remains a critical support system for millions of Americans. As of July 2025, more than 7.1 million disabled workers, along with hundreds of thousands of their spouses and children, received SSDI benefits. The average monthly benefit for disabled workers is $1,582, offering essential financial stability when health challenges limit the ability to work.

SSDI also comes with specific rules: in 2025, the Social Security Administration considers earnings above $1,620 per month for non-blind beneficiaries or $2,700 for those who are blind as “substantial gainful activity,” which could impact eligibility and benefit amounts.

So what happens if you want to work part-time while keeping your benefits? Many people assume they must choose one or the other. In reality, the SSA has programs designed to make this transition smoother. The Trial Work Period (TWP) gives beneficiaries nine months (spread across 60 months) to test the waters without losing benefits. As long as earnings in a “service month” exceed $1,160 in 2025, SSDI continues.

After the TWP, the Extended Period of Eligibility (EPE) provides a 36-month safety net. During that time, SSDI payments continue for months as long as earnings remain below the SGA threshold. If earnings exceed it, benefits stop only after a two-month grace period, but can restart whenever earnings drop back down. These rules create flexibility, letting people experiment with work without immediately losing their safety net.

Beyond the Paycheck

Part-time employment isn’t just about money. It can bring structure to your days, opportunities to connect with others, and intellectual engagement that keeps your skills sharp. Many people find that work provides a sense of purpose that extends beyond the financial aspect, whether it’s contributing to household needs, mentoring others, or pursuing a role that aligns with personal interests.

Returning to work can also rebuild confidence after a health setback. Small successes at work such as meeting deadlines, learning new tasks, or collaborating with a team can reinforce self-efficacy and independence. Social connections formed on the job can reduce feelings of isolation, offering both emotional support and a renewed sense of belonging. In short, part-time work can be a powerful step toward reclaiming control over your life and your daily rhythm.

Take the Next Step

At Four Leaf Financial, we partner with individuals and families navigating life’s transitions. Our clients come with diverse circumstances and goals, but they share a common desire: to make informed choices, maintain financial security, and explore opportunities without fear.

If you’re considering work while receiving SSDI, it’s worth having a conversation with someone who understands the nuances. With planning, you can test your limits, explore new opportunities, and work to keep your financial security intact.

Life doesn’t pause because of disability or fear, but with preparation, guidance, and a clear understanding of your options, you can step into work that feels right without sacrificing the benefits you rely on. Reach out today to start the conversation.

As we move through August, the economic landscape feels as chaotic as the aisles of a store stocked with Halloween decorations in the middle of summer. As a financial advisor and a parent, I’m feeling the pressure from both sides. On one hand, we have the ongoing uncertainty surrounding tariffs and their potential impact on the markets and the broader economy. The lack of clarity on who is being charged what creates a headwind for businesses and investors. On the other, while shopping for my college-bound sophomore, I was struck by the relentless push for consumption, a force that powers over 60% of our market’s performance. It’s a vivid reminder that our children are being raised in a society where the impulse to buy is constantly being triggered, whether in physical stores or online.

This juxtaposition presents a fascinating and complex challenge. Do I want tariffs to curb the flow of “junk” and encourage more mindful consumption, even if it risks market volatility? Or do I prioritize the market’s stability, which is so heavily dependent on the very consumer spending that can be so hard to control? The reality is that both of these forces—macroeconomic policy and individual spending habits—are deeply intertwined. Our job, as financial advisors and as parents, is to help our clients and children navigate this paradox. It’s about finding the balance between a healthy, growing economy and fostering the personal discipline to spend and save with intention. How do we, in a world of constant temptation, teach the next generation to control their impulses and build a foundation of financial wisdom?

Do you remember playing on a teeter totter at the park when you were younger? That constant shifting, trying to find the perfect balance? That is the image that comes to mind. As you read this those August days are slipping away. Make sure to get out there and enjoy the season before fall arrives.

On July 4, 2025, President Trump signed into law what he called the “One Big, Beautiful Bill” (OBBBA)—a sweeping piece of tax legislation that makes permanent many of the provisions from the 2017 Tax Cuts and Jobs Act (TCJA), while introducing several new changes that could impact families, business owners, and estate planning strategies.

Here are a few highlights:

Estate Planning: The unified estate and gift tax exclusion has been made permanent at $15 million per individual / $30 million per couple, indexed for inflation. (This is up from the ~$7M/$14M that would’ve taken effect without the bill.)

Higher Standard Deduction: For 2025, individual filers can claim $15,750 and married couples $31,500. Those 65+ may be eligible for an additional deduction, though it phases out at higher incomes.

SALT Deduction Expanded: Taxpayers earning under $500,000 in AGI can now deduct up to $40,000 in state and local taxes—up from the previous $10,000 cap.

Family-Friendly Credits: The child tax credit has been increased to $2,200 per child and made permanent, while the dependent care tax credit has also expanded. There’s a new “Trump account” for children born between 2025–2028: a tax-free savings account seeded with $1,000 by the federal government.

Small Business Benefits: OBBBA restores full first-year write-offs for equipment and R&D costs, along with enhanced deductions for pass-through entities.

Tax Planning: Why It Matters Now More Than Ever

With the signing of the OBBBA, tax planning has shifted from a “nice-to-have” to a financial must. As part of Four Leaf’s comprehensive financial planning services, I use a program called Holistiplan to review your tax return and work alongside your CPA or tax professional to help you prepare for what’s coming. The goal? To make the most of today’s rules and be ready for tomorrow’s.

What Is Tax Planning?

Tax planning is not the same as tax preparation. While your CPA or software like TurboTax helps you file your return correctly, tax planning is forward-looking. It’s a detailed review of your return to identify opportunities to reduce your lifetime tax liability.

Why Is It Important?

Because taxes touch every part of your financial life. Your tax return is like a financial fingerprint—unique to you and full of insight. A proactive review can uncover strategies you might otherwise miss, and help us have smarter, more personalized conversations about your future.

What Kind of Opportunities Might Be Identified?

Using Holistiplan, I evaluate a wide range of possibilities, such as:

Optimal timing of income and deductions

Strategies for Roth conversions

Charitable giving efficiencies

Tax bracket management

Impacts of changing filing status or dependents

How the sale of a business or exercise of stock options might affect your tax picture

Tax laws are changing in real time, making now the perfect opportunity to take advantage of the tax planning services already included in your relationship with Four Leaf Financial Planning.

Earlier this year, I found myself refreshing a webpage with shaky hands and a pounding heart. After months of studying, late nights, and more flashcards than I care to admit, the results of the Certified Financial Planner™ exam were in.

It was a relief, yes, but also something deeper. Pride, certainly. But even more than that, it was a feeling of stepping fully into a promise I’d already made: to show up for you with the highest standard of care, expertise, and ethics in your financial life.

If you’ve never worked with a CFP® before, you might wonder what the letters even mean or why they matter. Let’s talk about it.

The Gold Standard in Financial Planning

Anyone can call themselves a financial advisor. It’s an unregulated title, which means it doesn’t automatically signal training, testing, or accountability. The CFP® designation, on the other hand, does.

To earn it, candidates must complete rigorous coursework, pass a challenging exam, and demonstrate hundreds of hours of professional experience. The topics covered are wide-ranging, including retirement planning, taxes, insurance, investments, estate planning, and ethics, and the test itself is known for its difficulty. In March 2025, only 65% of nearly 4,000 test takers passed.

But passing the test is only part of the story. CFP® professionals also commit to ongoing education and, perhaps most importantly, to a fiduciary standard, meaning they are legally and ethically required to put your interests first.

Why That Matters in Real Life

So, what does this mean for you?

At Four Leaf, we work with people who are navigating real, often complex life moments. Maybe you’re planning for retirement and want to make sure your income lasts. Maybe you’re caring for a loved one with special needs and trying to understand how benefits, trusts, and long-term care planning fit together.

In these moments, surface-level advice isn’t enough. You deserve a partner who understands the whole picture and who has the training to guide you through it with clarity and care.

Having a CFP® means we’re not guessing or relying solely on instinct. We’re using a proven framework, backed by rigorous education and a code of ethics, to help you make confident, informed decisions.

More Than a Credential

The CFP® isn’t just a set of letters; it’s a mindset. It’s a way of approaching financial planning that prioritizes people over products and long-term trust over short-term gains.

It’s also a reminder that we’re always learning. Financial laws change. Life circumstances shift. What worked ten years ago might not make sense today. Being a CFP® involves staying up to date, ensuring that the advice we offer is not only thoughtful but also timely and accurate.

And here’s something else I think is important: just 24% of CFP® professionals are women. That gap matters. At Four Leaf, we believe representation makes financial guidance more accessible and personal. We show up as ourselves so you can, too.

A Partner You Can Trust

At the end of the day, working with a CFP® isn’t just about numbers. It’s about trust. It means you have someone in your corner who is trained to see the whole picture, listen deeply, and help you plan for a future that aligns with your goals and values. Whether you’re building a retirement strategy, creating a long-term care plan, or just figuring out where to begin, we’re here to walk alongside you.

Curious what that looks like in practice? Let’s talk. You bring your story. We’ll bring the expertise.

We understand that the emotional ups and downs related to market volatility are very real—especially when headlines about tariffs, trade wars, or economic uncertainty come at you fast and unfiltered.

As financial advisors—and as fellow humans—we’ve seen what uncertainty can stir up. It’s easy to feel rattled. But it’s also a great moment to take a breath, refocus, and remember that market movement is not a flaw of the system—it’s a feature.

Why Markets Move

When tariffs or other global policy changes dominate the headlines, the markets do what they always do: react. Behind every stock market shift are millions of buyers and sellers, each trying to make sense of what the news means for the future. We are seeing this play out in real time.

A series of tariff announcements sparked sharp declines in the market, followed by further dips as other nations, including China, responded in kind. The S&P 500 saw significant losses over just a few days, while volatility spiked and investor nerves were tested. But as the dust settled, the markets—as they often do—began to stabilize.

Volatility isn’t new. In fact, it’s something we plan for. Long-term investors know that movement—sometimes dramatic—is part of the deal. It’s not just a possibility, it’s an expectation.

Volatility Isn’t the Enemy

We know it’s uncomfortable to watch the market dip, especially after a stretch of strong performance. But volatility is also what allows for growth. It’s what creates opportunity. Markets rise and fall in response to the world around us, and those movements—while unpredictable in the short term—have historically trended upward over time.

At Four Leaf, we like to remind our clients that pullbacks and corrections aren’t necessarily a signal to act—they’re often a reminder to pause, reflect, and stay the course.

Timing the market—trying to guess when to jump in or out—is incredibly difficult, even for professionals. Often, the biggest gains come right on the heels of the biggest drops. Missing just a few of those strong days can have a significant long-term impact.

Staying Invested Matters

Imagine selling everything during a downturn to “wait it out.” Sounds reasonable, right? But the recovery often begins before you feel ready to re-enter. That means you could miss the rebound entirely. That’s why we encourage our clients to stick to their plan, even when the markets feel anything but predictable.

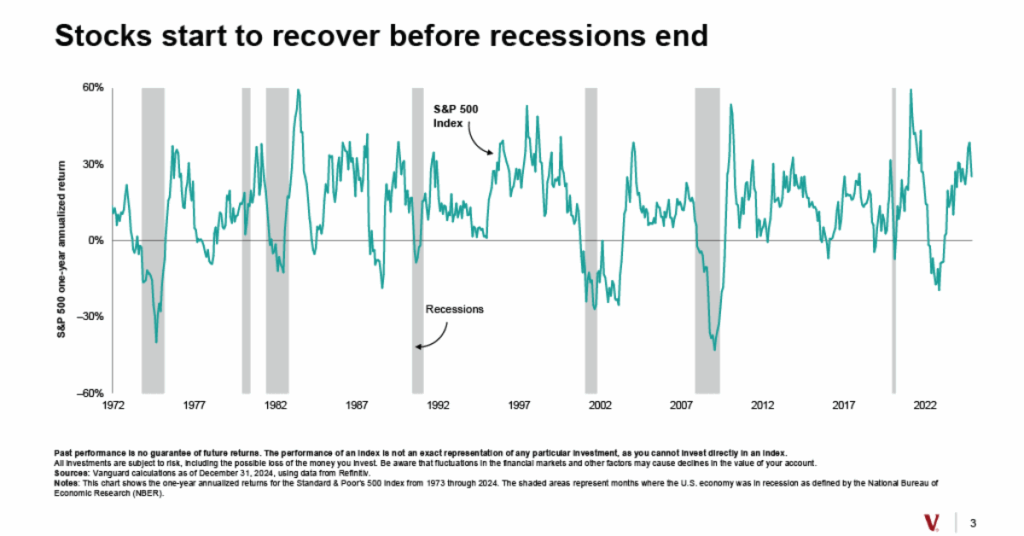

History backs this up. Markets have recovered from wars, recessions, pandemics, and political upheaval. Short-term discomfort has almost always given way to long-term growth. Staying invested, especially in a portfolio built around your goals and risk tolerance, is one of the best decisions you can make.

Your Portfolio Is Built for This

When we designed your portfolio, we knew days like this would come. That’s why it includes a mix of different asset classes—stocks, bonds, global exposure, and more. Diversification helps spread risk and cushion against volatility. While one part of your portfolio might dip during a downturn, another part might hold steady or even gain.

That’s not by accident. It’s by design.

And while we can’t prevent the markets from fluctuating, we can work with you to ensure your plan is built to withstand those fluctuations without losing sight of your long-term goals.

Looking Forward

Markets are inherently forward-looking. That means prices today reflect expectations for the future. Sometimes that leads to quick, dramatic moves based on developing stories—like changes in trade policy or global economic shifts.

SOURCE: Vanguard, Inc.

But those movements don’t always have lasting consequences. Historically, even during periods of stagflation (a combination of slowing economic growth and rising prices), markets have delivered positive returns more often than not. And even in the face of recessions, long-term investors who stayed invested have often been rewarded for their patience

We’re Here for You

We know it’s not easy to stay calm when the headlines are loud, and the numbers are flashing red. That’s why we’re here—not just to build your financial plan, but to walk with you through seasons of uncertainty.

If you’re feeling anxious, unsure, or just want to talk about how this all fits into your bigger picture, let’s connect. We’re happy to revisit your plan, run the numbers, and make sure you’re still on track. Spoiler alert: You probably are.

We’re here to listen, to guide, and to remind you that this journey—like all journeys—goes best with a steady hand and a clear head.

Sources: Vanguard, Inc. “Market Volatility,” 2025 update Dimensional Fund Advisors, “Tariffs and Stagflation,” February 21, 2025 National Bureau of Economic Research, “Business Cycle Dating”

Investment advisory services provided by Forefront Wealth Partners, LLC. Forefront also markets advisory services under the name, Four Leaf Financial Planning. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns.

Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful, or that markets will act as they have in the past.

We understand that the emotional ups and downs related to market volatility are very real—especially when headlines about tariffs, trade wars, or economic uncertainty come at you fast and unfiltered.

As financial advisors—and as fellow humans—we’ve seen what uncertainty can stir up. It’s easy to feel rattled. But it’s also a great moment to take a breath, refocus, and remember that market movement is not a flaw of the system—it’s a feature.

Why Markets Move

When tariffs or other global policy changes dominate the headlines, the markets do what they always do: react. Behind every stock market shift are millions of buyers and sellers, each trying to make sense of what the news means for the future. We are seeing this play out in real time.

A series of tariff announcements sparked sharp declines in the market, followed by further dips as other nations, including China, responded in kind. The S&P 500 saw significant losses over just a few days, while volatility spiked and investor nerves were tested. But as the dust settled, the markets—as they often do—began to stabilize.

Volatility isn’t new. In fact, it’s something we plan for. Long-term investors know that movement—sometimes dramatic—is part of the deal. It’s not just a possibility, it’s an expectation.

Volatility Isn’t the Enemy

We know it’s uncomfortable to watch the market dip, especially after a stretch of strong performance. But volatility is also what allows for growth. It’s what creates opportunity. Markets rise and fall in response to the world around us, and those movements—while unpredictable in the short term—have historically trended upward over time.

At Four Leaf, we like to remind our clients that pullbacks and corrections aren’t necessarily a signal to act—they’re often a reminder to pause, reflect, and stay the course.

Timing the market—trying to guess when to jump in or out—is incredibly difficult, even for professionals. Often, the biggest gains come right on the heels of the biggest drops. Missing just a few of those strong days can have a significant long-term impact.

Staying Invested Matters

Imagine selling everything during a downturn to “wait it out.” Sounds reasonable, right? But the recovery often begins before you feel ready to re-enter. That means you could miss the rebound entirely. That’s why we encourage our clients to stick to their plan, even when the markets feel anything but predictable.

History backs this up. Markets have recovered from wars, recessions, pandemics, and political upheaval. Short-term discomfort has almost always given way to long-term growth. Staying invested, especially in a portfolio built around your goals and risk tolerance, is one of the best decisions you can make.

Your Portfolio Is Built for This

When we designed your portfolio, we knew days like this would come. That’s why it includes a mix of different asset classes—stocks, bonds, global exposure, and more. Diversification helps spread risk and cushion against volatility. While one part of your portfolio might dip during a downturn, another part might hold steady or even gain.

That’s not by accident. It’s by design.

And while we can’t prevent the markets from fluctuating, we can work with you to ensure your plan is built to withstand those fluctuations without losing sight of your long-term goals.

Looking Forward

Markets are inherently forward-looking. That means prices today reflect expectations for the future. Sometimes that leads to quick, dramatic moves based on developing stories—like changes in trade policy or global economic shifts.

We understand that the emotional ups and downs related to market volatility are very real—especially when headlines about tariffs, trade wars, or economic uncertainty come at you fast and unfiltered.

As financial advisors—and as fellow humans—we’ve seen what uncertainty can stir up. It’s easy to feel rattled. But it’s also a great moment to take a breath, refocus, and remember that market movement is not a flaw of the system—it’s a feature.

Why Markets Move

When tariffs or other global policy changes dominate the headlines, the markets do what they always do: react. Behind every stock market shift are millions of buyers and sellers, each trying to make sense of what the news means for the future. We are seeing this play out in real time.

A series of tariff announcements sparked sharp declines in the market, followed by further dips as other nations, including China, responded in kind. The S&P 500 saw significant losses over just a few days, while volatility spiked and investor nerves were tested. But as the dust settled, the markets—as they often do—began to stabilize.

Volatility isn’t new. In fact, it’s something we plan for. Long-term investors know that movement—sometimes dramatic—is part of the deal. It’s not just a possibility, it’s an expectation.

Volatility Isn’t the Enemy

We know it’s uncomfortable to watch the market dip, especially after a stretch of strong performance. But volatility is also what allows for growth. It’s what creates opportunity. Markets rise and fall in response to the world around us, and those movements—while unpredictable in the short term—have historically trended upward over time.

At Four Leaf, we like to remind our clients that pullbacks and corrections aren’t necessarily a signal to act—they’re often a reminder to pause, reflect, and stay the course.

Timing the market—trying to guess when to jump in or out—is incredibly difficult, even for professionals. Often, the biggest gains come right on the heels of the biggest drops. Missing just a few of those strong days can have a significant long-term impact.

Staying Invested Matters

Imagine selling everything during a downturn to “wait it out.” Sounds reasonable, right? But the recovery often begins before you feel ready to re-enter. That means you could miss the rebound entirely. That’s why we encourage our clients to stick to their plan, even when the markets feel anything but predictable.

History backs this up. Markets have recovered from wars, recessions, pandemics, and political upheaval. Short-term discomfort has almost always given way to long-term growth. Staying invested, especially in a portfolio built around your goals and risk tolerance, is one of the best decisions you can make.

Your Portfolio Is Built for This

When we designed your portfolio, we knew days like this would come. That’s why it includes a mix of different asset classes—stocks, bonds, global exposure, and more. Diversification helps spread risk and cushion against volatility. While one part of your portfolio might dip during a downturn, another part might hold steady or even gain.

That’s not by accident. It’s by design.

And while we can’t prevent the markets from fluctuating, we can work with you to ensure your plan is built to withstand those fluctuations without losing sight of your long-term goals.

Looking Forward

Markets are inherently forward-looking. That means prices today reflect expectations for the future. Sometimes that leads to quick, dramatic moves based on developing stories—like changes in trade policy or global economic shifts.

SOURCE: Vanguard, Inc.

But those movements don’t always have lasting consequences. Historically, even during periods of stagflation (a combination of slowing economic growth and rising prices), markets have delivered positive returns more often than not. And even in the face of recessions, long-term investors who stayed invested have often been rewarded for their patience

We’re Here for You

We know it’s not easy to stay calm when the headlines are loud, and the numbers are flashing red. That’s why we’re here—not just to build your financial plan, but to walk with you through seasons of uncertainty.

If you’re feeling anxious, unsure, or just want to talk about how this all fits into your bigger picture, let’s connect. We’re happy to revisit your plan, run the numbers, and make sure you’re still on track. Spoiler alert: You probably are.

We’re here to listen, to guide, and to remind you that this journey—like all journeys—goes best with a steady hand and a clear head.

Sources: Vanguard, Inc. “Market Volatility,” 2025 update Dimensional Fund Advisors, “Tariffs and Stagflation,” February 21, 2025 National Bureau of Economic Research, “Business Cycle Dating”

Investment advisory services provided by Forefront Wealth Partners, LLC. Forefront also markets advisory services under the name, Four Leaf Financial Planning. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns.

Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful, or that markets will act as they have in the past.

The start of a new year brings fresh opportunities to reassess your financial goals and align them with the latest updates in contribution limits, tax thresholds, and savings opportunities. For 2025, several key limits have increased, offering expanded opportunities to maximize savings and reduce your tax burden.

By understanding and leveraging these annual updates, you can make informed decisions to strengthen your financial future. Let’s explore these changes in more detail and discuss why it’s essential to pay attention to these numbers each year.

IRA Contribution Limits

In 2025, the contribution limit for traditional and Roth IRAs has increased to $16,500, with an additional $3,500 catch-up contribution available for those aged 50 and older and $5,250 for those ages 60-63.

Why It Matters: IRAs are a cornerstone of retirement planning. For traditional IRAs, contributions may be tax-deductible, reducing your taxable income for the year. Roth IRAs, on the other hand, allow for tax-free growth and withdrawals in retirement, provided you meet certain criteria.

Even if you’re already contributing to an employer-sponsored plan like a 401(k), IRAs provide additional savings flexibility and diversification. With higher limits, you can put even more toward your retirement goals, helping to secure your financial future.

401(k) Contribution Limits

For 2025, the 401(k) contribution limit has risen to $23,500, with an additional $7,500 catch-up contributionfor those 50 and older and $11,250 for those 60-63. This means individuals over 50 can contribute up to $30,500 or more in total.

Why It Matters: Employer-sponsored plans like 401(k)s are often the backbone of retirement savings for many individuals. Not only do these accounts allow for significant tax-deferred savings, but many employers also match contributions, which is essentially “free money” toward your retirement.

Contributing the maximum amount—or as much as you can comfortably afford—not only builds your nest egg but also reduces your taxable income. For higher earners, this can make a significant difference in your annual tax liability.

Health Savings Accounts (HSAs)

If you’re enrolled in a high-deductible health plan (HDHP), the HSA contribution limit for 2025 has increased to $4,300 for individuals and $8,550 for families. Those aged 55 and older can also make an additional $1,000 catch-up contribution.

Why It Matters: HSAs are a triple-tax-advantaged savings tool: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are also tax-free.

For individuals planning for retirement, HSAs can act as a powerful savings vehicle for healthcare costs, which are often among the most significant expenses in retirement. Unlike flexible spending accounts (FSAs), HSA funds roll over year to year, allowing you to build a substantial balance over time.

Estate and Gift Tax Exemptions

The federal estate tax exemption for 2025 has increased to $13,990,000. Additionally, the annual gift tax exclusion is now $19,000 per recipient, up from $17,000 in 2024.

Why It Matters: These changes present an opportunity for strategic wealth transfer. Whether you’re making annual gifts to loved ones or planning for the transfer of your estate, these updated limits can help reduce your overall tax burden.

Gifting up to the annual exclusion amount allows you to transfer wealth without using your lifetime exemption or incurring gift taxes. For those with significant estates, this strategy can be part of a larger plan to minimize future estate taxes and preserve more of your wealth for the next generation.

Why It’s Crucial to Stay Updated

Every year, these limits are adjusted to account for inflation and changes in tax policy. Staying informed ensures you’re taking full advantage of all available opportunities to save, reduce taxes, and protect your wealth.

For example:

Missing out on increased contribution limits could mean losing the chance to grow your savings faster.

Failing to manage gift taxes or estate plans effectively might leave more of your wealth exposed to unnecessary taxes.

Overlooking tools like HSAs or Roth IRAs can result in missed opportunities for tax-efficient savings.

By reviewing these changes annually, you can adjust your financial plan to make the most of what’s available to you.

Take the Next Step: Get the Full List of 2025 Limits

At Four Leaf Financial Planning, we’re committed to helping you stay informed and ahead of the curve. To simplify your planning, we’ve compiled all the important annual limits for 2025 into one convenient PDF.

Take this opportunity to set yourself up for a successful year. If you’re ready to discuss how these updates fit into your financial plan, let’s connect. Together, we’ll make 2025 a year of progress and financial growth.

As a financial advisor at Four Leaf Financial Planning, I’ve had many conversations with clients surprised by how quickly healthcare costs can add up in retirement. These expenses are often unpredictable and can significantly impact your retirement savings if not appropriately planned. But with thoughtful preparation, you can take control of your healthcare costs and avoid unnecessary financial stress.

Let’s explore how you can plan for healthcare costs before and after age 65, manage tax liabilities, and stay ahead of potential expenses like Medicare premiums and long-term care.

Before 65: Tackling Healthcare Costs with the Affordable Care Act (ACA)

If you retire before 65, you may rely on ACA marketplace plans for health insurance. Here’s what to know:

Premiums Are Income-Based: Your modified adjusted gross income (MAGI) determines your eligibility for subsidies. Keeping your income within certain limits can reduce your monthly premiums significantly.

Costs Vary by Age and Location: Premiums generally rise with age and can differ widely depending on where you live.

Strategies to Manage ACA Premiums

Adjust Your Income: Stay within 400% of the federal poverty level to qualify for ACA subsidies. Thoughtful withdrawals from retirement accounts can help you stay under this threshold.

Use Health Savings Accounts (HSAs): These accounts offer a triple tax advantage—tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses.

Plan Roth Conversions Early: Strategically converting funds to a Roth IRA before retirement can minimize taxable income and keep your ACA premiums low.

At 65: Transitioning to Medicare

Once you turn 65, Medicare becomes your primary coverage, but it’s not free. Understanding the structure and costs of Medicare is essential for budgeting:

Medicare Part A (Hospital Insurance): Typically premium-free if you’ve worked at least 10 years.

Medicare Part B (Medical Insurance): Upon turning 65, Medicare becomes your primary health insurance. In 2025, the standard Part B premium is $185 per month, up from $174.70 in 2024.

Medicare Part D (Prescription Drugs): Costs depend on your plan and medication needs.

The Impact of IRMAA (Income-Related Monthly Adjustment Amount)

If your MAGI exceeds certain thresholds, you’ll face higher premiums for Medicare Parts B and D. This surcharge is based on your income from two years prior, making proactive tax planning critical to avoid surprises. Higher-income beneficiaries may pay additional premiums for Parts B and D. For 2025, IRMAA surcharges apply to individuals with MAGI above $106,000 and couples above $212,000.

Tax Planning to Optimize Healthcare Costs

Effective tax strategies can help you manage healthcare expenses, from ACA premiums to Medicare IRMAA charges:

Use Roth IRA Withdrawals: Roth distributions don’t count toward your MAGI, making them an excellent source of tax-free income.

Consider Qualified Charitable Distributions (QCDs): If you’re over 70½, QCDs from your IRA can satisfy required minimum distributions without increasing taxable income.

Plan Income Recognition Carefully: Spread large withdrawals over multiple years to avoid bumping into higher tax brackets or IRMAA tiers.

Planning for Major Expenses and Long-Term Care

Healthcare inflation and long-term care are two factors that can derail even the best financial plans. Here’s how to stay prepared:

Long-Term Care Insurance: Medicare doesn’t cover long-term care, and costs can be substantial. Purchasing insurance early can provide valuable protection.

Combat Inflation with Growth Investments: Keeping part of your portfolio in growth-oriented assets can help your savings keep pace with rising healthcare costs.

Stay Proactive: Regularly update your financial plan to account for changes in healthcare costs, ensuring your savings remain on track.

Why It Pays to Plan Ahead

Healthcare expenses are a significant part of retirement, but with proactive planning, you can manage these costs effectively. By understanding how ACA premiums, Medicare, IRMAA, and taxes interact with your finances, you can maintain control and protect your hard-earned savings.

At Four Leaf Financial Planning, we specialize in helping retirees navigate these complexities. Let us help you create a comprehensive plan that addresses your healthcare needs and ensures a more secure and enjoyable retirement.

Note: This information reflects 2025 figures and policies as of the latest updates. For personalized advice, consult with a financial advisor.

As you plan for retirement, every decision you make now can significantly impact your financial future. One of the most pressing questions you might be facing is whether to execute a Roth conversion, especially with the expiration of the Tax Cuts and Jobs Act (TCJA) on the horizon. Let’s dive into what this means for you and whether a Roth conversion could be right for you.

Understanding the TCJA and Its Expiration

The Tax Cuts and Jobs Act passed in 2017, brought about some of the most substantial changes to the tax code in recent history. It lowered income tax rates, doubled the standard deduction, and capped certain itemized deductions, among other things. These changes have allowed many taxpayers to enjoy reduced tax liabilities over the past few years.

However, unless Congress extends it, the TCJA will expire on December 31, 2025. When it does, tax rates are expected to revert to their pre-2018 levels, meaning higher taxes for many people. This potential increase has many individuals, like yourself, wondering whether they should lock in today’s lower tax rates through strategies like a Roth conversion.

What Is a Roth Conversion?

Before deciding, it’s crucial to understand what a Roth conversion entails. If you have money in a traditional IRA or 401(k), that money has been growing tax-deferred—meaning you haven’t paid taxes yet. When you withdraw it in retirement, you’ll owe taxes at your ordinary income tax rate at that time.

A Roth conversion allows you to transfer some or all of that money into a Roth IRA. In doing so, you’ll pay taxes on the converted amount now at today’s tax rates. However, once the funds are in the Roth IRA, they grow tax-free, and when you withdraw them in retirement, you won’t owe any taxes on those withdrawals. It’s essentially paying taxes now to avoid paying them later.

Why You Might Consider a Roth Conversion Before the TCJA Expires

There are several reasons why a Roth conversion could be particularly appealing before the TCJA expires:

Locking in Lower Tax Rates: With the possibility of tax rates increasing after 2025, converting now allows you to pay taxes at today’s lower rates. This conversion could save you a significant amount in taxes compared to waiting until after the TCJA expires.

Tax-Free Growth: Your money can grow tax-free once you invest in a Roth IRA. Any investment gains, dividends, or interest earned within the account will not be subject to taxes, maximizing your retirement savings.

No Required Minimum Distributions (RMDs): Roth IRAs don’t require you to take distributions at age 72, unlike traditional IRAs. This time duration gives you more flexibility to let your money grow tax-free for as long as you like, potentially leaving more for your heirs.

Flexibility in Retirement: Since Roth IRA withdrawals are tax-free, you’ll have more control over your taxable income in retirement, which can help you manage your tax bracket and avoid higher taxes on Social Security benefits or Medicare premiums.

What Are the Downsides?

While a Roth conversion offers several potential benefits, it has its drawbacks. Here are a few considerations to keep in mind:

Upfront Tax Cost: Converting to a Roth IRA requires paying taxes on the amount converted. Depending on the size of your conversion, this could result in a significant tax bill. Make sure you have the cash available to cover this cost without dipping into your retirement savings.

Impact on Other Financial Goals: Paying taxes now could impact other areas of your life. It might leave you with less money for other priorities, like saving for a child’s education, buying a home, or building an emergency fund.

Potential for Higher Medicare Premiums: A large Roth conversion could push you into a higher tax bracket for the year, which might increase your Medicare premiums. It’s important to carefully plan the amount you convert each year to avoid unintended consequences.

State Taxes: Don’t forget about state taxes. Depending on where you live, your Roth conversion could be subject to state income taxes, which could add to the overall cost.

Should You Move Forward?

So, should you proceed with a Roth conversion before the TCJA expires? The answer depends on your unique situation. It’s not just about the numbers—it’s about your goals, your plans for the future, and your comfort level with paying taxes now for the benefit of tax-free income later.

If you’re considering a Roth conversion, it might be wise to discuss it with a financial advisor. They can help you weigh the pros and cons and determine whether it’s the right strategy for you. Remember, the decisions you make today will shape your retirement tomorrow. Take the time to explore your options and make the choice that best aligns with your vision for the future.

At Four Leaf Financial Planning, we’re here to help you navigate these decisions. If you’re considering a Roth conversion or want to explore other strategies to maximize your retirement savings, schedule some time with Kathleen or download our Roth Conversion Q&A Guide to answer some important questions.

")

")